Five essential risk management strategies for your practice

Avant media

Thursday, 11 November 2021

Managing your clinical and business risk is an essential part of good governance, helping create trust in your staff, your patients and community. The pandemic has highlighted the increased need for risk mitigation strategies, from telehealth versus in-person consultations to vaccination programs and infection control. As doctors and heads of medical practices, you play a critical role in managing risk well.

What is risk management and how can it help your practice?

Catherine Maxwell, General Manager for Policy and Advocacy at Governance Institute of Australia defines it as, “strategies to identify and manage the threats your practice faces, but also to manage and leverage uncertainty for the benefit of your practice.”

These strategies form part of a greater risk framework, which outlines your practice’s overall approach to risk. Risk can also present opportunities for your practice to grow, such as improving your care quality, or offering new treatments or expertise.

To help you improve your practice’s risk management so you continue to deliver high-quality healthcare and explore opportunities for growth, here are five essential strategies to implement:

1. Create a detailed risk management framework

Include elements such as:

- a statement of your practice’s commitment to managing risk

- desired outcomes of your risk management framework

- a list of the types or categories of risk

- your risk appetite, and how you assess, respond to and report risk

- your risk management process – a step-by-step format is ideal

- staff roles and responsibilities in managing risk.

2. Categorise the types of risk applicable to your practice

Typical healthcare practice risk categories include:

- strategic risk: external risks that may impact your plans for growth

- operational risk: internal risks impacting your daily operations, such as the computer system breaking down

- cyber risk: such as privacy and data breaches, damage to digital files, malware and cyber extortion

- financial: cash flow, credit and debt issues

- legal and compliance: claims and disputes, Medicare, Ahpra and ATO compliance risks

- clinical risk: missed diagnosis, incorrect medications and failure to follow up results etc.

3. Set your risk appetite

Risk appetite is the amount and type of risk a business is prepared to take on in pursuit of a goal. This is separate to ‘risk tolerance’, which refers more to the level of risk (low, medium, high).

Your risk appetite needs to align to your strategic objectives because it will drive how you do business and what risks your business will take. It will also depend on the size and governance structure of a practice. While large and small practices may have similar risk appetites around clinical practice, regulation and governance, they may differ around financial and innovation risk. That’s why agreement amongst leadership is important when setting your risk appetite, so leaders can be guided by the agreement.

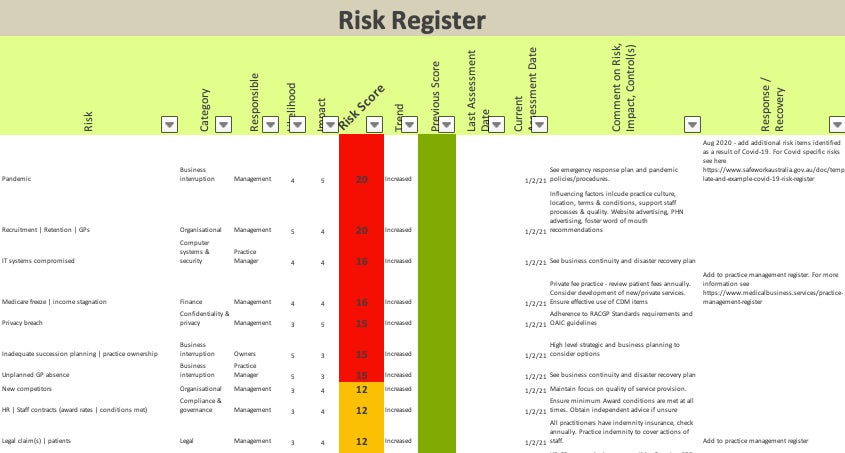

4. Develop a risk register and audit process

When you have a sense of the risks your practice faces and have ranked them by severity, you can plan to be better prepared for them. Riwka Hagen, Principal Consultant of Medical Business Services, suggests creating a risk register. This can be a simple spreadsheet, documenting the following details:

- risk

- category

- who is responsible

- likelihood score

- impact score

- overall risk score (likelihood compared to impact)

- trend (increased, stable or decreased)

- previous score

- last and current assessment dates

- comments

- response/recovery.

She also recommends regular audits of your highest risk areas that can result in patient harm or significant business impact.

5. Encourage a risk-aware culture

A risk-aware culture sets expectations around team behaviour and how they translate your risk management framework into decisions that manage and mitigate risk. How do you create a risk-aware culture?

- Assess your current culture: Consider a staff survey or discussion in meetings to determine your risk culture.

- Identify what ‘good’ looks like for your practice: Leaders need to agree on expectations and behaviours to then model these for the team.

- Build risk management capability: Set employees up for success in managing risk. This may involve revising job descriptions to add certain risk responsibilities.

- Monitor and review: This ensures your risk culture continues to meet your overall strategy as your practice grows.

When you include risk management in your everyday decision-making, you foster a culture of open, no-blame communication, which encourages all staff to play their part as risk managers.

Find out how Avant can support your practice to improve risk management. Visit the Avant website or call 1800 128 268.

Disclaimers

IMPORTANT: This publication is not comprehensive and does not constitute legal or medical advice. You should seek legal or other professional advice before relying on any content, and practise proper clinical decision making with regard to the individual circumstances. Persons implementing any recommendations contained in this publication must exercise their own independent skill or judgement or seek appropriate professional advice relevant to their own particular practice. Compliance with any recommendations will not in any way guarantee discharge of the duty of care owed to patients and others coming into contact with the health professional or practice. Avant is not responsible to you or anyone else for any loss suffered in connection with the use of this information. Information is only current at the date initially published.